Upcoming new accounting rules will affect what your bottom line will look like.

Part 3 of 3

Part 1: 5 Things You Need to Know About New Accounting Rules for Commercial Real Estate Leases

Part 2: 4 Steps to Preparing for New Accounting Rules on Commercial Real Estate Leases

New accounting rules for commercial real estate leases, including your Tucson office lease, will change your bottom line, affecting your ability to attract investors and get bank loans. It could also affect the amount of taxes you pay.

Even though the proposed rules won’t go into effect until Jan. 1, 2019 for public companies and Jan. 1, 2020 for private companies, now is the time to talk with your financial advisor or commercial real estate tenant representative. They can help you figure out how to put yourself in the best financial position possible.

New Accounting Rule

Briefly, the new accounting rules will require you to record all commercial real estate leases that are at least 12 months long on your balance sheet as an up-front liability at the start of the lease.

Instead of recognizing a lease as an operating lease or a capital lease, you’ll need to classify the lease as

- Type A leases, effectively a sale or financing. Leases currently classified as capital leases are likely to be Type A leases.

- Type B leases, essentially the same as operating leases under the current rules. Office building, retail and other standard commercial real estate leases classified as operating leases under current rules are likely to be Type B leases under the new rules.

Short-term vs. Long-term Leases

You may think the simple solution is to negotiate only a short-term office lease and renewal option.

With a shorter lease term, the new right-to-use-the-property (ROU) asset and future lease payment liability that you’ll have to record on your balance sheet at the start of the lease will be smaller.

Be careful. The short-term lease strategy won’t work for all tenants.

You shouldn’t use it if significant construction is planned for the space. Any reductions in the ROU asset are likely to be wiped out by higher amortization costs over the initial lease term.

Getting a renewal option to extend the amortization period won’t solve the problem. That’s because extending the amortization period gives you “a significant economic incentive” to exercise the option.

That will put you over the 12-month lease definition under the new accounting rules. In essence, the renewal option plus incentive to exercise turns the lease into a longer term lease, effectively undoing the short-term lease strategy.

Then you have to count future lease payments during the renewal period in calculating the ROU asset.

Of course, there’s more to leasing than accounting. If you’re in retail or another business in which staying in one location is crucial, minimizing the ROU asset may be less significant than the stability of a long-term lease.

5 Office Lease Strategies to Protect Your Company

1. Understand how the new balance sheet reporting requirements affect you.

This is crucial when you’re negotiating a commercial real estate lease.

You need to consider

- whether the lease you’re negotiating is Type A or Type B

- how the lease’s economic terms will be reflected as assets, liabilities, revenues and costs on your financial statements.

2. Shift costs to non-reportable expenses.

The value of the ROU asset recognized on the balance sheet is the present value of future lease payments, including

- fixed rent

- variable lease payments pegged to an index or rate

- residual value guarantee payments.

You can reduce the value of the ROU asset by shifting payment obligations to payments that don’t count, like variable payments based on sales, performance or usage of the asset such as CAM and other operational expenses.

3. Make leases triple net.

One of the best ways to shift future lease payments to non-reportable operating costs is via a triple net lease. You agree to pay fixed rent and a pro rata share of CAM, insurance and taxes.

Make sure that operating cost payments are based on actual costs rather than adjustments against a base year. Lease payments become reportable when they’re tied to an index or rate.

4. Make the owner commit to financial transparency.

New rules require you and the owner to recognize the initial value of the ROU asset and reassess it to reflect significant economic changes. So require the owner to

- monitor the relevant variables, such as the index or rate to which a particular lease payment is pegged

- notify you of changes

- provide the data you need to make your own reassessments.

5. Structure leases as Type B, not Type A.

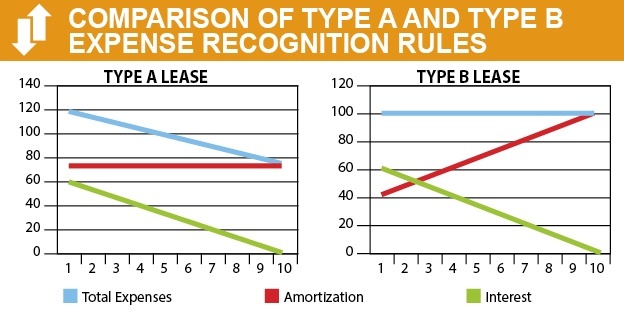

Although both types of leases must be recognized on the balance sheet in the form of the bloated ROU asset, the P&L recognition rules for Type B are kinder and gentler. They let you combine amortization and interest expense as a single lease cost on a straight-line basis.

Although both types of leases must be recognized on the balance sheet in the form of the bloated ROU asset, the P&L recognition rules for Type B are kinder and gentler. They let you combine amortization and interest expense as a single lease cost on a straight-line basis.

Structuring leases as Type B enables you to avoid the dreaded front-loaded, downhill interest expense slope that must be shown on the Type A P&L.

Share your experiences on working with Commercial Real Estate Group of Tucson.