A four-step process can get put you in compliance with the new rules.

Part 2 of 3

Part 1: 5 Things You Need to Know About New Accounting Rules for Commercial Real Estate Leases

Part 3: 5 Ways to Protect Your Commercial Real Estate Lease in a New Accounting Climate

New accounting rules that may go in effect as early as Jan. 1, 2019 for public companies and Jan. 1, 2020 for private companies will change how your commercial real estate lease costs are reported.

You will be required to record all leases that are at least 12 months long on your balance sheet as an up-front liability at the start of the lease.

That could affect your ability to attract investors and qualify for loans. It will also affect how much you pay in business taxes.

How to Comply With the New Accounting Rules

Step 1: Determine if your lease is covered.

Your lease falls under the new accounting rules if it is

- at least 12 months long

- shorter than 12 months, gives you an option to renew the lease or purchase the property and you are “reasonably certain” to exercise the option in light of all the economic factors.

Step 2: Classify the lease as Type A or B.

If your lease is covered, you must figure out what type of lease it is. There no longer will be operating leases and capital leases. Instead, commercial real estate leases will be classified as either

- Type A leases, effectively a sale or financing. Leases currently classified as capital leases are likely to be Type A leases.

- Type B leases, essentially the same as operating leases under the current rules. Office building, retail and other standard commercial real estate leases classified as operating leases under current rules are likely to be Type B leases under the new rules.

Step 3: Properly account for the lease on your balance sheet.

You must record Type A and B leases on the balance sheet at two different times, initial recognition and reassessment.

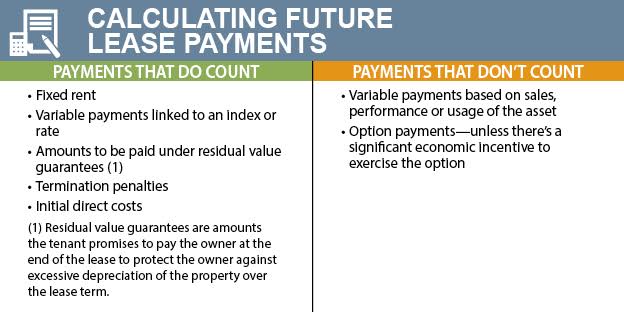

Initial Recognition. When the lease begins, you will need to list a new asset called right to use the property (ROU). This reflects the present value of  future lease payments over the lease term.

future lease payments over the lease term.

Include your initial direct costs in relation to the ROU asset. Also make sure you know what future lease payments do and don’t count.

You’ll also need to include the value of a lease liability.

You must present your Type A and Type B lease ROU assets and liabilities as separate line items on your balance sheet or in the notes to your balance sheet.

Reassessment. Over the course of the lease, you’ll have to reassess the value of lease payments you reported, as well as the discount rate you used to calculate their present values. The reassessment reflects lease modifications and other important changes affecting

- the term of the lease caused by a significant event or change in circumstances that are within your control

- variable lease payments based on an index or rate to the extent you decide to re-measure the ROU liability for other reasons

- the discount rate you used to calculate the ROU asset in response to changes in the lease term or your option to purchase the property.

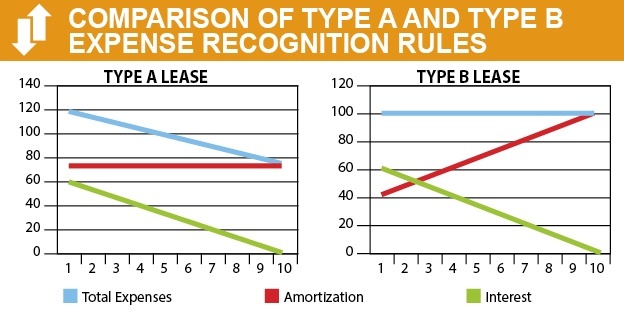

Step 4: Properly account for lease expenses on your income statement.

As under current rules, you’ll have to account for all lease-related expenses on your income statement, also called a P&L. You must recognize

- amortization of the ROU asset—that is, the amount by which the asset’s value is reduced as it’s consumed over the lease term

- interest expense related to the lease liability.

While the lease-related expenses are the same for both types of leases, there are important differences in the method you use to recognize them on the P&L.

Type B lease: Combine the amortization and interest on a Type B lease into a single lease expense that you recognize on a straight-line basis over the course of the lease.

Type A lease: Treat amortization and interest on a Type A lease as separate costs. That’s a big deal because while amortization costs are straight-line, interest expenses are higher in the early

years of the lease and decrease over time.

The result of this “front-loading” is that you’ll have to recognize significant interest costs on your P&L when you enter into a Type A lease. Those added P&L expenses could affect your paper profitability and harm your standing with investors and creditors.

Share your experiences on working with Commercial Real Estate Group of Tucson.